Why Being Blind Beats 99% of VCs

The Humble Guide | Insight Piece #2

Of the 14 models we evaluate across seven empirical datasets, none is consistently better than the 1/N rule in terms of Sharpe ratio, certainty-equivalent return, or turnover, which indicates that, out of sample, the gain from optimal diversification is more than offset by the estimation error . . . That is, the effect of estimation error is so large that it erodes completely the gains from optimal diversification.

Translated in plain English, this seminal study by researchers at London Business School, found that a "1/N" strategy dominates every other investment strategy in stock investing.

What is a 1/N strategy?

Also known as an equally-weighted strategy, the 1/N strategy allocates 1/N percentage to each of the N stocks in an N-stock investment portfolio.

For example, a 1/N strategy allocates 10% equally for each stock in a 10-stock portfolio.

Simple enough, but could it be possible that the 1/N strategy is also optimal for early-stage investing in Venture Capital?

Power Laws in Venture Capital

Well, let's take a step back to fundamentals.

Have you ever wonder why VCs often pass on startups – even if they're developing something truly innovative and sustainable – because they're not "VC investable?"

What does VC investable actually mean?

It has to do with something called the Power Law Rule.

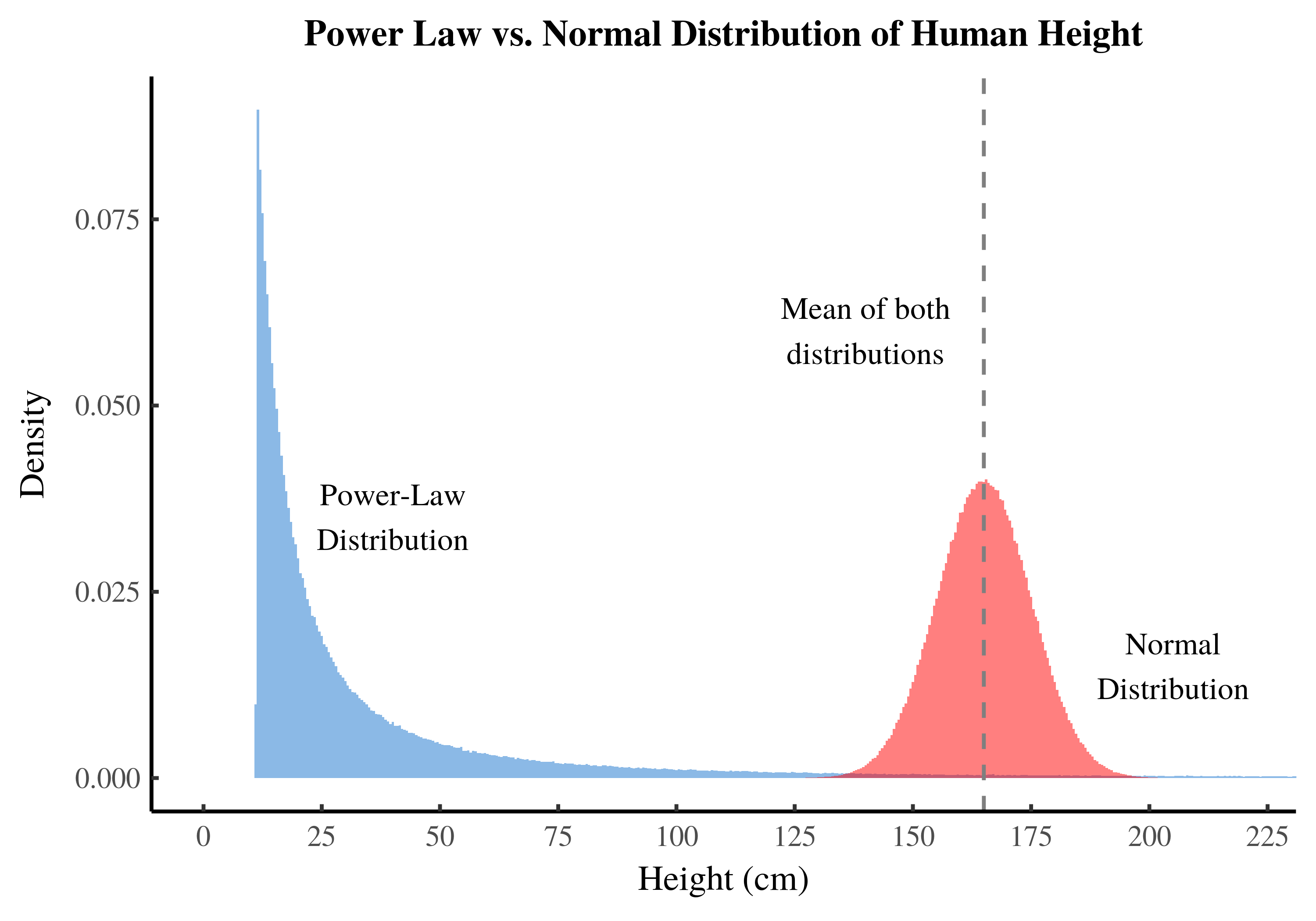

Source: Blair Fix; Example of a Power Law Distribution versus the commonly found Normal Distribution shown in the Frequency of Human Height.

The idea is that because early-stage investing is inherently risky, Venture Capitalists expect 9 out of every 10 startups to fail, with only one succeeding out of the ten.

Without diving into the Math of Venture Capital, this means that every startup investment is expected to return at least the entire fund size.

For a $100 million VC fund, half of it will be invested (the remainder for follow-ons), leaving $50 million, which divided among 10 companies yields a $5 million investment size.

This means every startup is expected to deliver at least a 20X gross return for the fund to just breakeven—a conservative estimate as this doesn't include the VC's investment fees.

Returning to the power law distribution—it represents the frequency profile of investment returns among the VC's startups, and is positively skewed because of the low success rate.

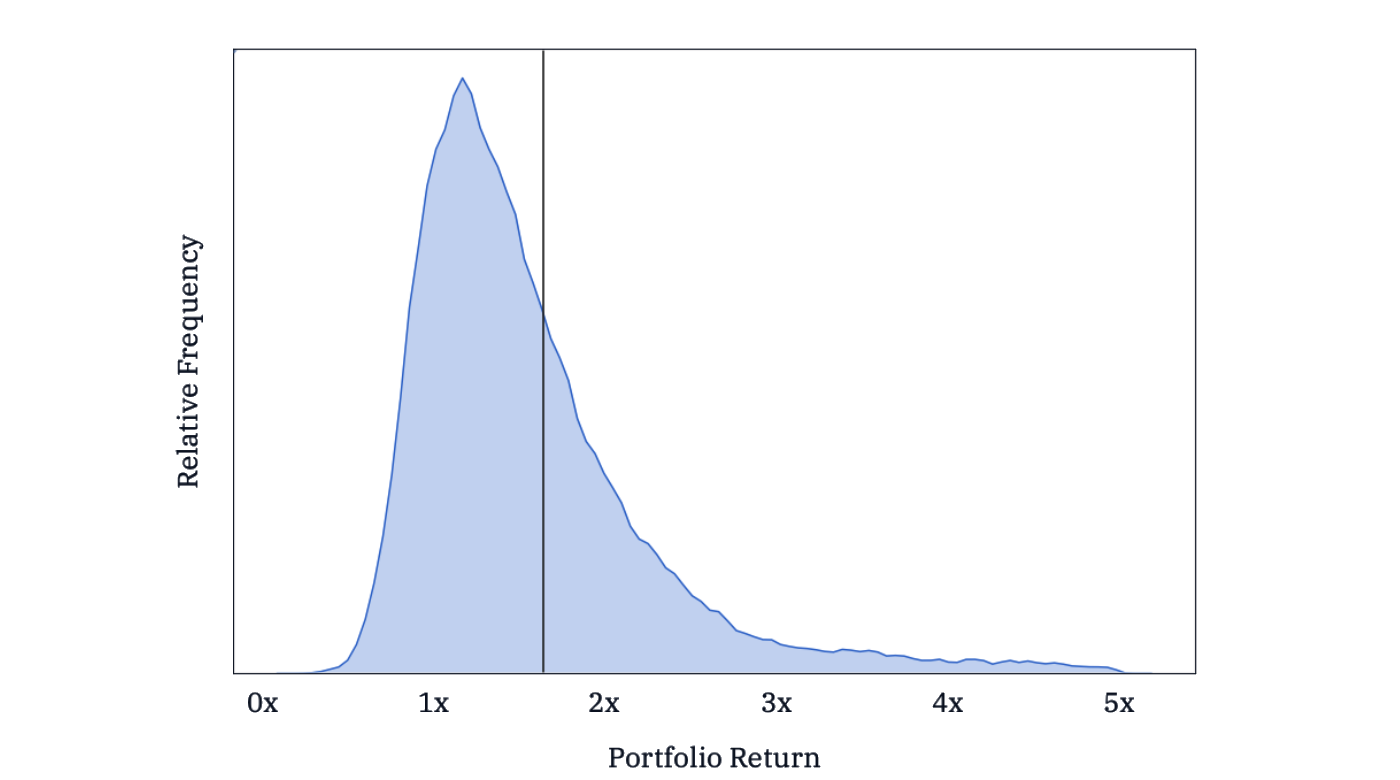

And this is exactly what AngelList – one of the largest early-stage investment platform – found by analyzing the thousands of startups that have been funded on their platform.

Source: AngelList; The black vertical line represents the market return, which is based on the 1/N strategy, and the peak of the curve represents the most frequently observed outcome from a 10-investment portfolio.

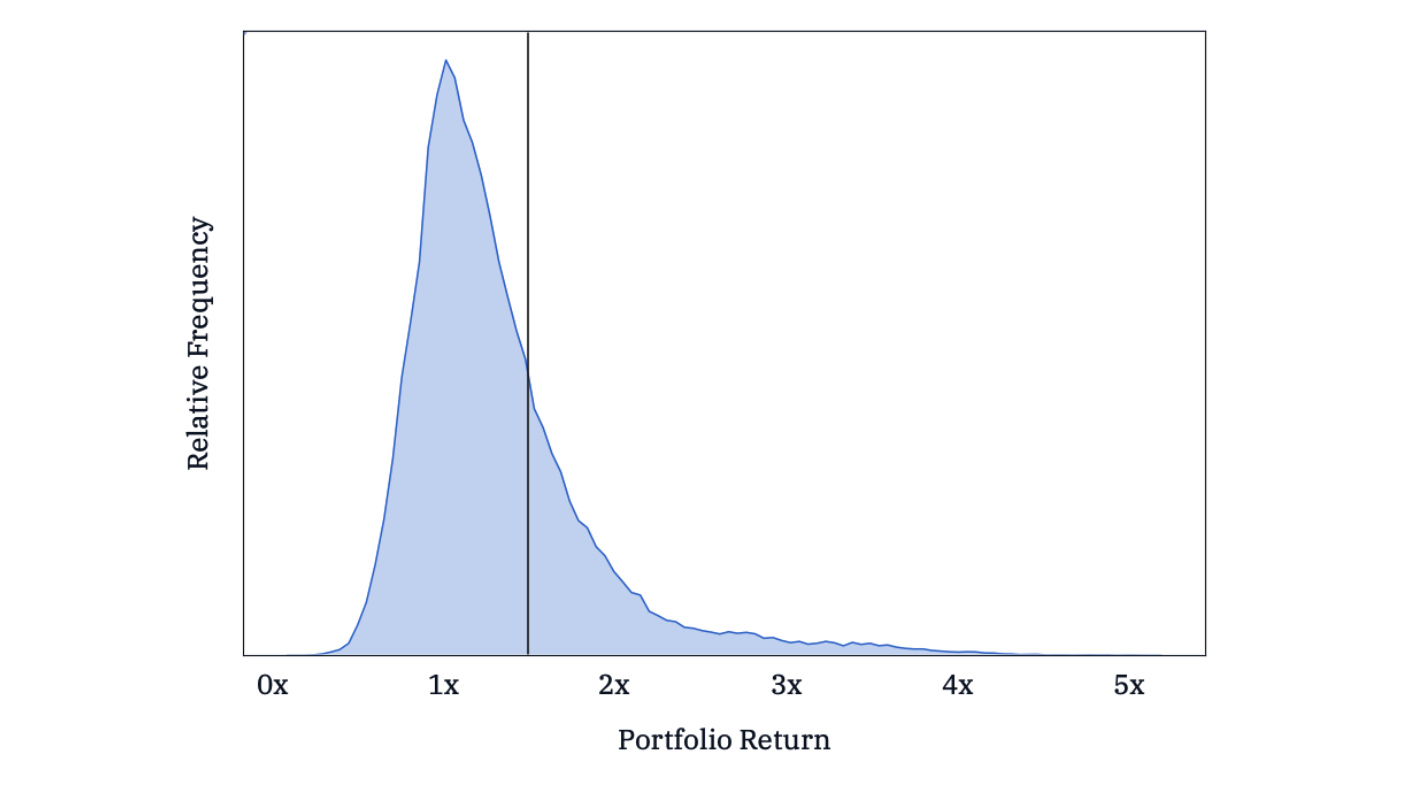

And this assumes no investment fees. With fees, the picture gets worse as expected.

Source: AngelList; The black line is again the market return of the 1/N strategy, and the probability (the shaded area) of a VC beating the market return has shrunk exponentially due to the 2/20 fees charged by the VC.

Being Blind Beats 99% of VCs

What is even more remarkable, is that by simulating over 50,000 hypothetical venture portfolios based on real-life fund data collected over a decade, AngelList shows that a simple 1/N portfolio outperforms a VC fund that misses investing in the best-performing seed investment.

You read that right: by missing out on the best-performing seed investment, the VC is almost doomed to underperform to say a simple allocation to an S&P 500 ETF.

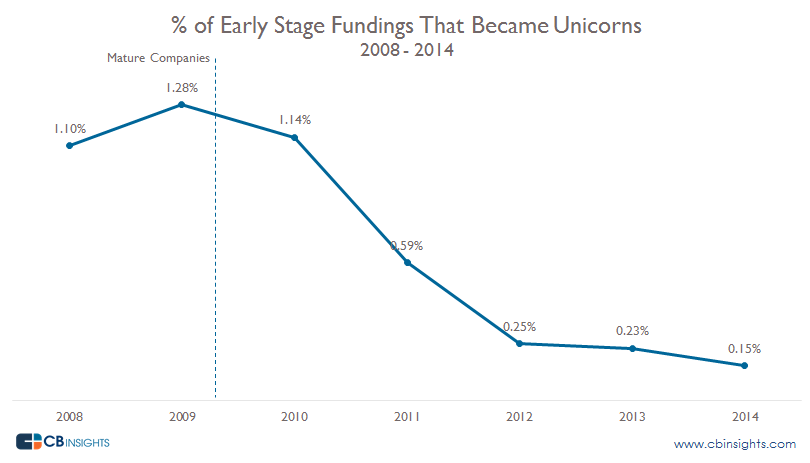

An extensive CB Insight report revealed that the probability of VC startup becoming a Unicorn (the "conversion rate") is about 1%, implying that the 1/N equally-weighted strategy would beat 99% of VC investors.

Source: CB Insights; Percentage of Early Stage Fundings that Became Unicorns from 2008 to 2014 is about 1% on average.

1/N might sound like a dumb and simplistic investment strategy, and while it's certainty simple, it's definitely not dumb.

Nobel Laureate Harry Markowitz – the Founder of Modern Portfolio Theory – agrees and uses this exact 1/N strategy for investing his own money, eschewing his own complicated theory in favor of this simpler approach.

"Instead, I visualized my grief in the stock market went way up and I wasn't in it–or if it went way down and I was completely in it. My intention was to minimize my future regret. So I split my contributions 50/50 between bonds and equities."

—Harry Markowitz

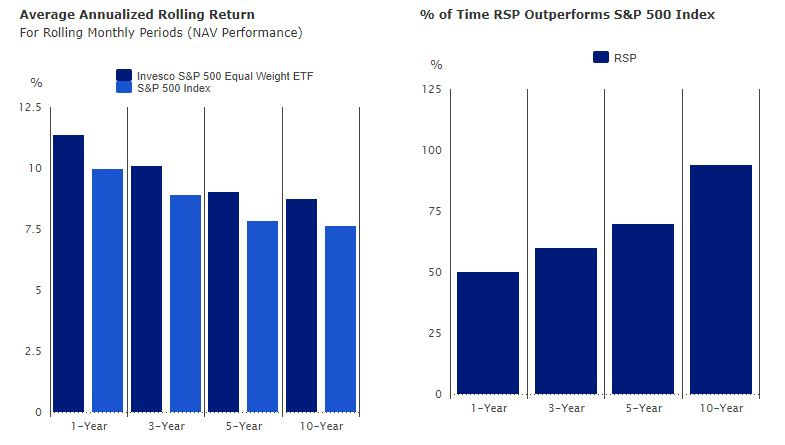

Again, empirical data also supports this thesis with abundant studies in the ETF / passive investing space demonstrating that an equally-weighted, 1/N strategy consistently outperforms a traditional market-cap strategy for broad-based exposure.

Source: Invesco, FactSet Research; Historical Outperformance of an Equally-Weighted 1/N ETF (RSP) tracking the S&P 500 Index versus the Market-Cap Weighted S&P 500 Index.

All this said I would hesitate to jump to the conclusion that Venture Capital has limited value for the average investor.

Obviously, there are exceptional VCs out there who have demonstrated a consistent track record of attracting exceptional Founders, building and scaling early-stage companies, and positioning these companies for a successful exit.

No one can deny this.

It's just that identifying and getting access to the Top 1% of those VCs is a Herculean task—with the understanding that the "Top 1%" by its very nature is an unknowable unknown.

In summary, the AngelList report concludes that:

"Conventional investing wisdom tells us that VCs should pass on most deals they see. But our research indicates otherwise: At the seed stage, investors would increase their expected return by broadly indexing into every credible deal."

If you're an asset owner invested in venture capital funds, maybe you should now reconsider what the "innocuous" management fee is really paying for?

Final Thoughts

Although these empirical findings may appear contrary to the propaganda promulgated by such publications like TechCrunch, Fast Company, and even the Wall Street Journal, they reveal the truth behind an industry that is more marketing than investing.

In the words of Marc Andreessen – Founder of VC Firm A16Z – one of his primary influences for launching his eponymous venture fund came directly from Hollywood.

Thus, it should not be surprising that A16Z primarily invests in social media networks and consumer startups where "hype marketing" plays a critical role in their successes, similar to how media hype and celebrity casting are used to promote a new blockbuster movie.

A16Z's fund performance leaked by investors/LPs to The Information reveals subpar returns net-of-fees, which adds to the plethora of existing literature that Silicon Valley is Broken.

Let's hope there is a new breed of early-stage investors like Capital, Republic, and Aidoswho are developing novel approaches to facilitating the funding of early-stage companies so that investors can have a much better investment outcome than a blind one.

By Andrew Vo

Editor of The Humble Guide

About The Humble Guide

The Humble Guide is a new kind of publication that cuts through the noise of venture capital and technology. Learn what really matters from a thought leader with over a decade of experience in finance, technology, and early-stage investing.

👉 If you enjoyed reading this post, feel free to share it with friends!

To read more content like this every week, subscribe to The Humble Guide 👇