The Management Guide to Decentralized Finance

The Humble Guide | Insight Piece #4

21 years ago, in 1999, Ethan Rasiel published The McKinsey Way.

This book quickly became a "must-read" for business school students and anyone applying to work in the management consulting industry as it shares insider tips into what it is like to work for "The Firm."

Although the McKinsey Way very much demystifies the process of management consulting at McKinsey, I can't possibly claim this guide will do the same for the emerging industry known as Decentralized Finance or DeFi.

However, I will share with you my insider tips having worked 10+ years in finance and having advised many Blockchain and FinTech startups at the DeFi intersection point.

Let's first take a step back in time to October 31, 2008.

From Byzantine to Bitcoin

On this innocuous date, an entity going by the name of Satoshi Nakamoto published a paper titled "Bitcoin: A Peer-to-Peer Electronic Cash System" that may be the most influential paper per word in recent memory.

For in a mere eight pages, Satoshi Nakamoto provided a solution to an unsolved problem known as the "Byzantine Generals Problem."

What in the world is the Byzantine Generals Problem?

More importantly, what does this have to do with Blockchain and DeFi?

Let me be brief without getting into the technical details.

The Byzantine Generals Problem is a fundamental problem faced by decentralized networks, which are networks (e.g, BitTorrent, insect colonies, and market economies) where there is no established Trust which can be found in say bank-to-consumer networks.

The Byzantine Generals Problem was first theorized by mathematicians Leslie Lamport, Marshall Pease, and Robert Shostak to find malfunctioning components that give conflicting information to other parts of a computer system.

The generals are a metaphor for nodes in a decentralized network, and the underlying idea is how to determine a peer-to-peer, distributed network with no central authority can make correct decisions, even if some of its nodes turn rogue.

In other words, can we make a distributed system that is “Trustless" and doesn’t automatically assume that the participants are going to act ethically, and work in the best interest of the group (an idea complementary to Adam Smith's "invisible hand")?

Solving this problem was the key hurdle to the creation of Bitcoin (and by extension, all other cryptocurrencies) and the exponential growth of Blockchain technology.

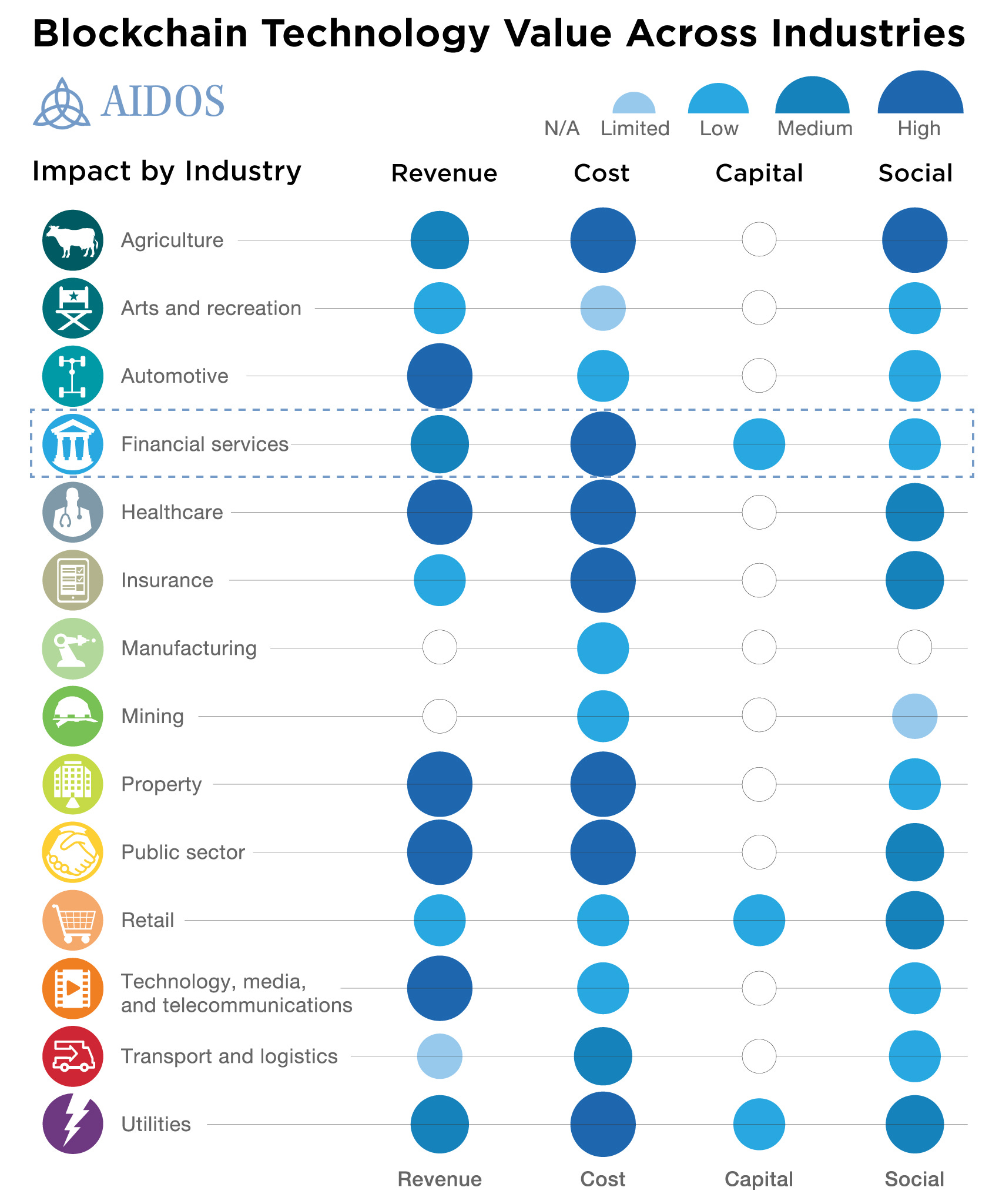

McKinsey and Company did extensive study of 90 use cases of across 14 different industries and found that Financial Services (i.e., Decentralized Finance) is one of just three industries (the other two being Retail and Utilities) where Blockchain will have an immediate impact across the key metrics (revenue, cost, capital, and social) they identified.

Source: McKinsey and Company; Blockchain Technology Value Across Industries.

Great, what is the role of Blockchain relative to Decentralization?

Blockchain as the Enabling Technology for Decentralization

Amidst all the noise of Bitcoin, ICOs, blockchain ventures like Consensys, and cryptocurrency investors like A16Z, I find it most helpful from a management perspective to think of Blockchain simply as an Enabling Technology.

For example, when Steve Jobs announced the launch of the iPhone in 2007, he timed it perfectly as he knew that the enabling cellular technology was then sufficiently matured to handle the data bandwidth of a Smartphone.

I would also point the reader to the fact that Decentralization is not just confined to any industry (say finance) but expands into many aspects of our society including the rise of Decentralization in the Workplace.

Source: Aidos Inc.; The Rise of Decentralization for Better Technology Adoption in the Workplace.

Although centralized, hierarchical organizations are the norm, I expect the emergence of decentralized companies like Illinois Tool Works, which was featured by Forbes in 1999 for leveraging autonomous units to help isolate production problems.

Indeed, with the COVID-19 pandemic, many tech companies like Twitter, Facebook, Google, and Uber have fully embraced remote working, which may lead to secular changes towards more decentralized corporate structures.

Let's now re-shift our focus to finance.

Since the inception of modern banking, developed nations like the U.S., U.K., Sweden, and Switzerland have relied on a number of well-capitalized financial institutions and regulatory bodies to serve as the foundational "trust layer."

Given the staggering importance of the financial services industry (representing $4.6 Trillion of the $21 Trillion US annual GDP ), many financial intermediaries have emerged in every conceivable layer whose roles have been to extract "rents" from the ecosystem, yet they lack incentives to innovate historically.

Contrary to popular opinion, the goal of DeFi is not to "replace" these financial intermediaries, but to provide users with a more competitive offering, which equates to lower transaction costs and prices.

Great, where do we start?

DeFi in Emerging vs. Developed Markets

When evaluating DeFi, the first bifurcation as you're developing your mental model, is to understand the difference of Decentralized Finance for Emerging vs. Developed Markets.

Source: Aidos Inc.; Role of Blockchain is Different for Emerging vs Developed Markets.

Within Developed Markets where banking and investment services are available to almost everyone, DeFi is more pertinent for providing liquidity to existing markets, reducing transaction costs (e.g., asset management commissions, secondary trading costs), eliminating intermediary fees (e.g., banking fees), and improving data accountability and reliability (i.e., an immutable, traceable book of records).

For example, Americans paid $34 Billion in overdraft fees in 2018, yet the average checking account balance is just shy of $3,400. We can only imagine these numbers have only gotten worse since the recession precipitated by the COVID-19 pandemic.

That said, most Americans are still wary of cryptocurrencies like Bitcoin and Ethereum, and even more are wary of Facebook's new "Libra" cryptocurrency.

In contrast, for Emerging Markets like the Philippines – a country where 77 percent of its citizens are unbanked – more than 5 million Filipinos (or 10 percent of the country's adult citizens) are using cryptocurrency exchanges as their primary method of payment.

Across the Pacific Ocean in Venezuela – a country with a history ripe with political corruption and hyperinflation – citizens have become wary of their own currency so the adoption of cryptocurrencies like Bitcoin (although not perfect) provide a more stable alternative for storing money.

Thus, the use cases for emerging markets are distinct from that of developed markets, a point that must be scrutinized if you're managing an international operation and exploring the incorporation of blockchain technology within your organization.

The aphorism "Think Globally, Act Locally" is quite relevant in this context.

So, how big this opportunity set?

DeFi Total Addressable Market

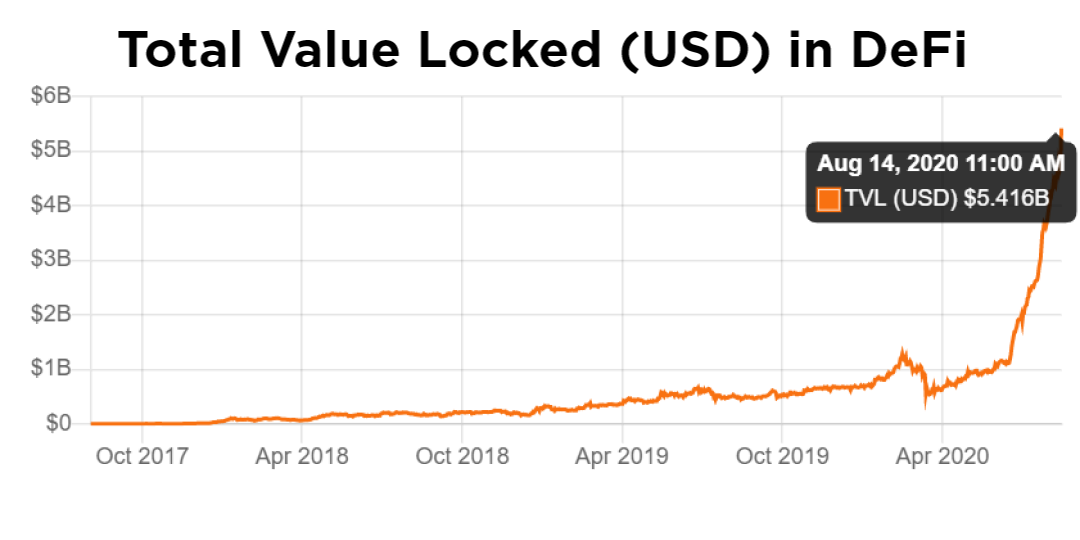

A useful metric for understanding the Total Addressable Market for Decentralized Finance is the idea of Total Value Locked or TVL.

TVL relies on the fact that most DeFi applications require capital to be deposited, often in the form of loan collateral or liquidity in a trading pool - hence the "locked up value."

While not a perfect metric by any means, TVL provides a useful indicator as it is somewhat analogous to Assets under Management or AUM when quantifying the total addressable market for the investment management industry.

As of August 14, 2020, the TVL in DeFi broke the $5 Billion level, having grown almost 8X since the start of 2020 from a TVL of just under $700 million.

Source: DeFi Pulse; Total Value Locked (USD) in DeFi from Aug-2017 to Aug-2020.

With Bitcoin having gained more than 60% over the same time period and gaining momentum, the DeFi market is poised for further expansion over the coming years.

So what are the key horizontal industries in DeFi?

I am often asked this question by VCs and FinTech Founders and my usual response is to divide the DeFi market into four categories: (1) Asset and Wealth Management, (2) Banking, Payments & Lending, (3) Capital Markets, and (4) Insurance.

In order to help you execute your firm's Digital Assets Strategy, the structure of each of these sections will revolve around mapping Blockchain solutions to representative "Disruptors" (nimble startups) and "Incumbents" (well-capitalized, larger companies).

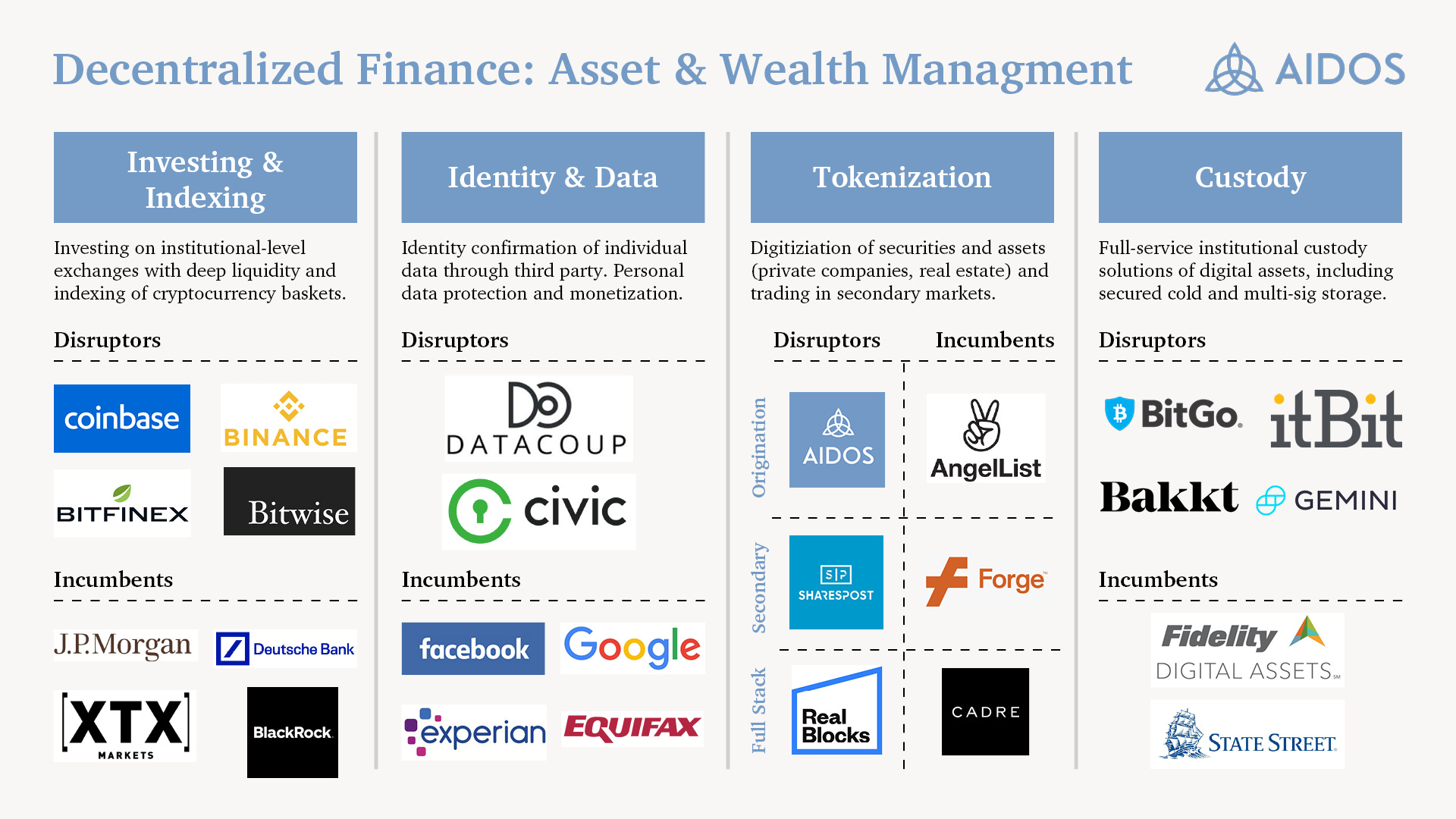

(1) DeFi for Asset and Wealth Management

Having worked at J.P. Morgan Asset Management as a portfolio manager for large institutional asset owners (e.g., pensions, endowments, and foundations), I understand first-hand the multi-faceted issues where Blockchain can have an immediate impact.

First, within Investing and Indexing, J.P. Morgan was an early mover among the "bulge bracket banks" in building out its distributed ledger technology / DLT known as Quorum. That said, I expect a pickup in M&A activity of startups (say for firms like Binance and Consensys) as banks are seeking to expand their DLT practice.

Source: Aidos Inc.; Decentralized Finance Mapping for Asset & Wealth Management.

Moving to Identity and Data, this is especially top-of-mind for many financial firms given the recent Equifax data breach of 147 million people, and the resulting $425 million settlement by the Federal Trade Commission. Datacoup and Civic are two innovative startups that promise to allow consumers to recapture their data sovereignty.

Tokenization is an especially disruptive idea for the $85 Trillion Global Asset Management industry as it promises to allow the democratization of investment assets, especially for illiquid assets like real estate, private equity funds, and even private market companies. Disruptors in this space include RealBlocks (for real estate investing), Sharespost (for secondary transactions), and Aidos (for startup investing).

Of the four industries within Asset and Wealth Management, Custody remains the most entrenched with the Top 3 Custodians (BNY Mellon, State Street, and J.P. Morgan) accounting for close to $66 Trillion of custodied assets globally.

By its very nature, this is where Blockchain technology can play a key role in reducing asset custodial costs, with Bakkt and Gemini both offering "institutional-level" custody services.

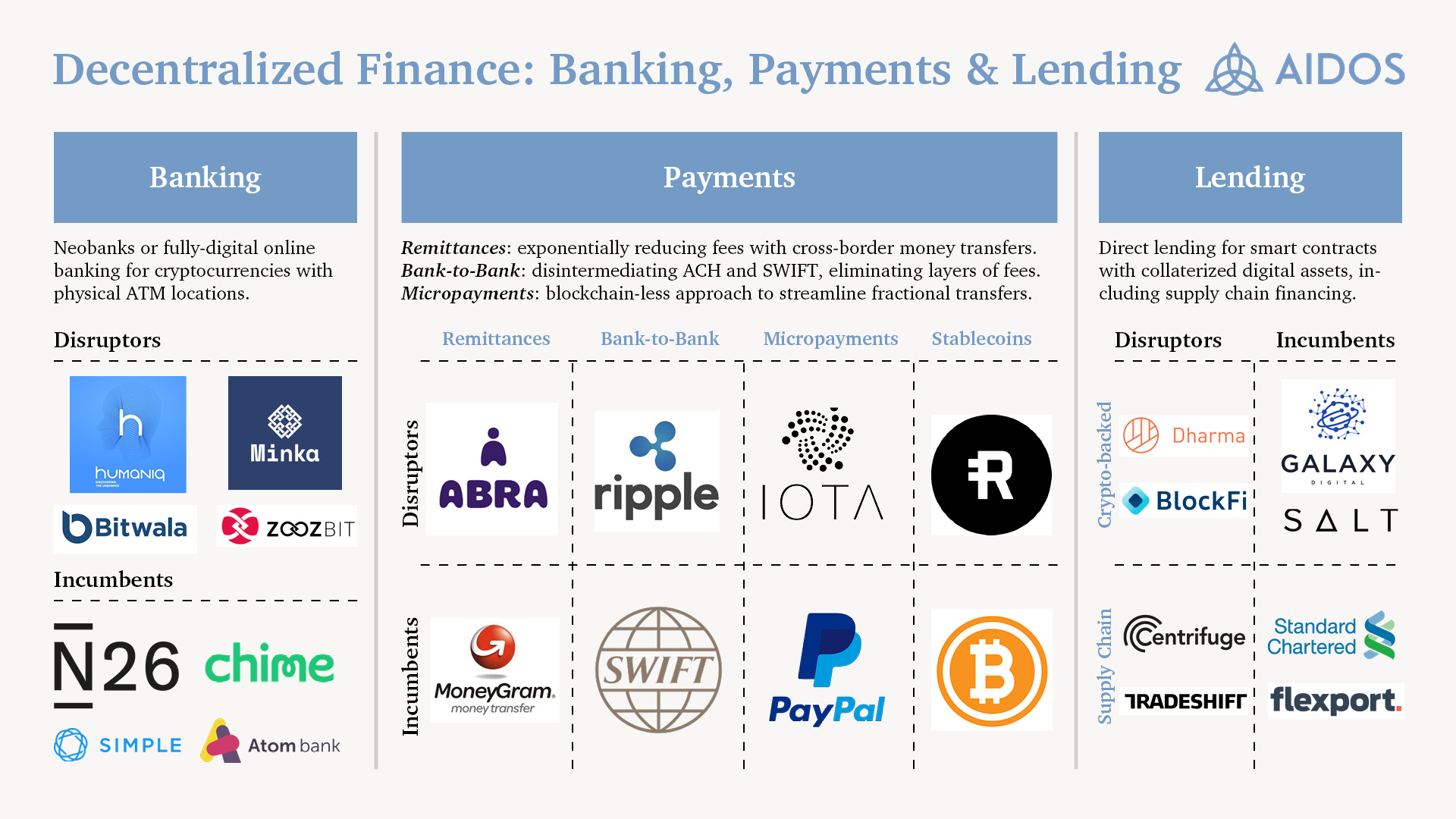

Moving to Banking, Payments, and Lending, arguably where the most immediate opportunities of Decentralized Finance lie.

(2) DeFi for Banking, Payments, and Lending

Having lived and worked in the "Crypto Valley" - a region just outside of Zurich, Switzerland where many innovative Blockchain startups have emerged - Banking is an area where Blockchain has made much progress in competing with existing financial platforms.

Indeed, cryptocurrencies have gotten so popular in Switzerland that there is a large number of BitCoin ATMs throughout the country, with Millennials now opting to make payments in cryptocurrencies than in cash, a trend that has been catalyzed by the COVID-19 pandemic.

Neobanks (also known as internet-only or digital banks) have emerged dedicated solely to cryptocurrencies with Humaniq, Minka, Bitwala, and ZoozBit gaining recent traction, with Humaniq (Africa) and Minka (Colombia) targeting the 1.7 Billion Adults globally who are underbanked.

Source: Aidos Inc.; Decentralized Finance Mapping for Banking, Payments, & Lending.

A recent report forecasted the Global Digital Remittance Market to reach $34 Billion by 2026, with the vast majority of remittances going to developed countries like the U.S., Switzerland, Germany, France, and Italy.

Indeed, ACH and SWIFT – the two dominant methods for transferring money globally, and which have changed little in decades – are slowly being disintermediated by startups like Abra and Ripple.

Micropayments startups like IOTA – transactions at fractions of a dollar – and Stablecoins – cryptocurrencies designed to minimize price volatility – like Reserve are gaining momentum, with Reserve now gaining the attention of senior officials at the European Central Bank (ECB).

Since the "Crypto Winter" of late 2018, Lending has been a particularly active area of the DeFi universe providing momentum for Crypto-backed startups like Dharma and BlockFi and Supply Chain startups Centrifuge and Tradeshift.

In order for the DeFi Lending market to grow sustainably, this requires a healthy and transparent Capital Markets.

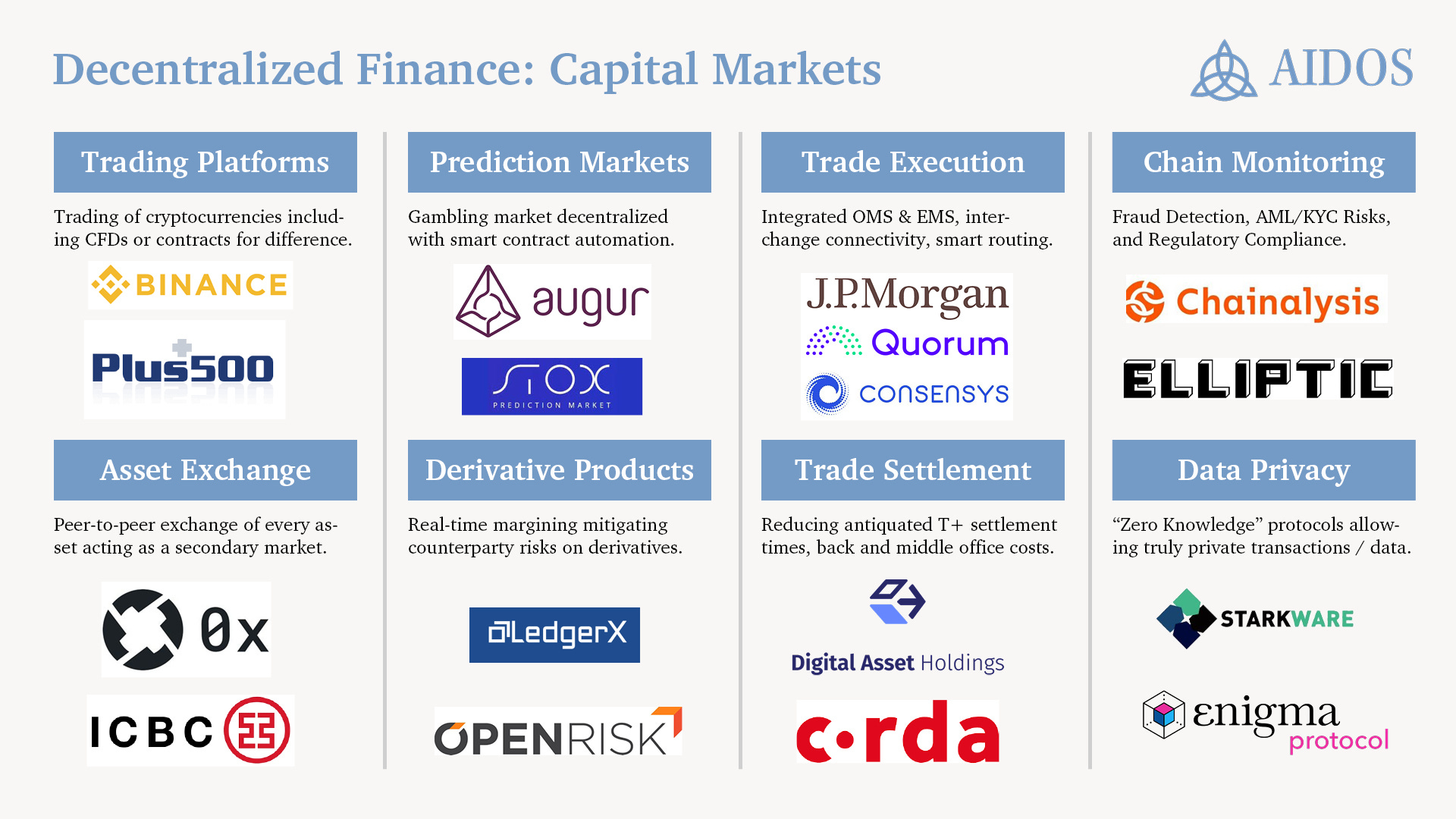

(3) DeFi for Capital Markets

Establishing a solid foundation for the Capital Markets within Decentralized Finance will be critical for adoption by Institutional Investors like Pensions, Sovereign Wealth Funds, Endowments, and Foundations.

Innovative Trading Platforms allowing for CFDs (contracts for difference) like Plus500 are gaining momentum in Europe, which is complemented by the expansion of Prediction Markets with startups like Augur and Stox competing in this arena.

Source: Aidos Inc.; Decentralized Finance Mapping for Capital Markets.

Within Asset Exchange – which serves a secondary, peer-to-peer market – we see an interesting DeFi corporate strategy being played out, one where ICBC (China's largest commercial bank) is developing its own solution in-house, while startups like 0x are pushing forth with their own trading platform.

Along the line of Clayton Christensen's Innovator's Dilemna, it remains to be seen whether ICBC's in-house strategy will win over an "outsource and M&A" strategy of acquiring startups similar to a corporate venture capital model.

Any well-functioning Capital Markets require strong Trade Execution and Trade Settlement. Of note, J.P. Morgan's blockchain unit Quorum is in talks to merge with Consensys, an Ethereum-based platform for blockchain business integration.

It's astounding that it took almost 40 years for the U.S. to reduce its "T+3" trade settlement requirement a single day to "T+2" in 2017. DeFi startups like Digital Asset Holdings seeks to eliminate this archaic policy altogether and will reduce back- and middle-office costs.

Last but not least, Chain Monitoring and Data Privacy are two areas where Blockchain technology really shines as transaction history is completely traceable on the "blockchain." Not surprisingly, the 17-year old responsible for the recent "Twitter Hack" was quickly apprehended due to this inherent feature of the Bitcoin blockchain.

We expect startups like Chainalysis and Elliptic for chain monitoring and data privacy protocols like Enigma to be an area of active development in the coming years.

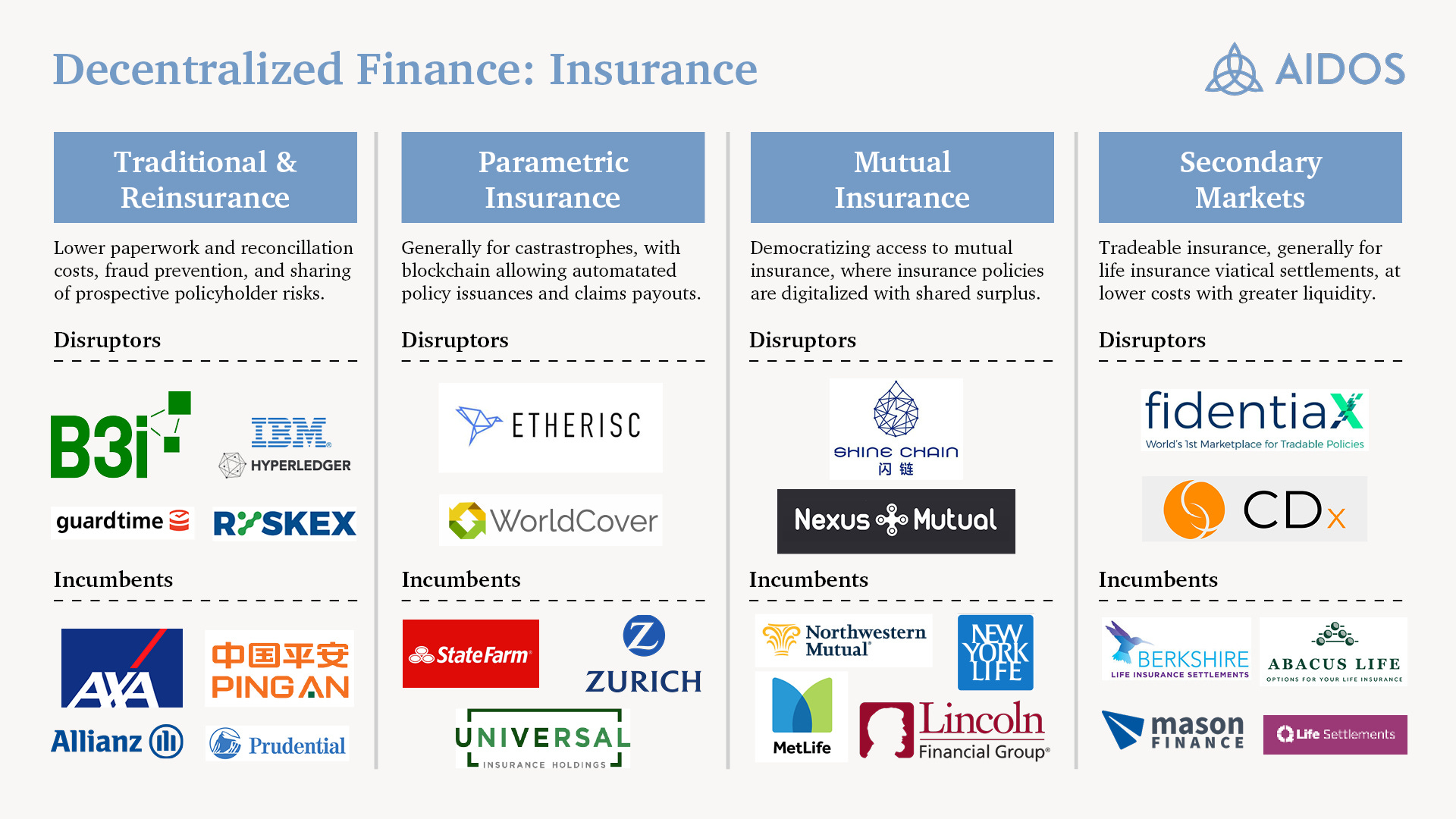

(4) DeFi for Insurance

Perhaps the most entrenched area in finance is Insurance, with a recent study showing that only 65 percent of the $1 Trillion in annual global insurance premiums actually goes to pay out claims, with the remaining $350 Billion going to administration costs, insurance brokers, and corporate profits.

Although there is some overlap with the InsurTech industry – which raised $1.6 Billion in new funding just in Q2 of 2020 alone – Insurance DeFi is distinct in that it's seeking to automate many of the manual and subjective aspects of the insurance product life cycle.

Source: Aidos Inc.; Decentralized Finance Mapping for Insurance.

Indeed, Traditional Insurers and Reinsurers are being disrupted by startups like B3i and Guardtime which seeks to lower paperwork and reconciliation costs, reduce fraudulent claims even allow sharing of risks by policyholders.

Parametric Insurance – an insurance contract where claims are paid automatically based on a triggering event – is an area ripe for competition by startups like Etherisc and WorldCover, with blockchain allowing for automated policy insurances in addition to claims payouts.

Mutual Insurance – an insurance structure that is popular in the U.S. and Canada – is gradually seeing some interest with startups like Shine Chain and Nexus Mutual promising to provide digitized policies with automatically shared surplus distributions.

Finally, the Secondary Markets for insurance – generally in the form of "viatical settlements" – is seeing moderate traction with DeFi platforms like fidentiaX trying to upend old incumbents like Abacus Life and Q Life Settlements.

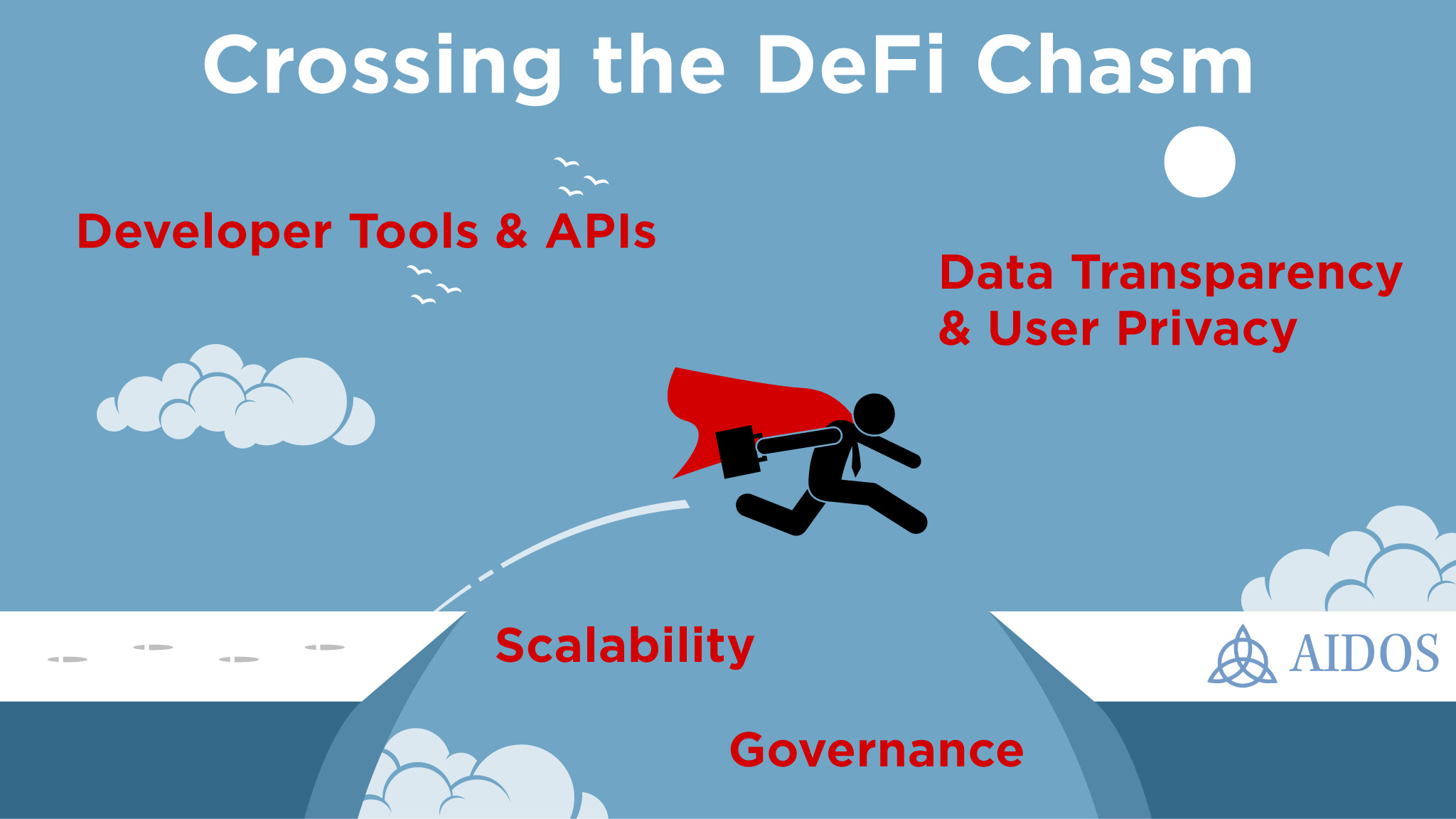

Crossing the DeFi Chasm

In "Crossing the Chasm" – Geofrey Moore's classic book for entrepreneurs – the chasm exists because after a certain point of selling a product to early adopters, sales will reach plateau where the next stage of growth is to the take the product to the masses.

I believe Decentralized Finance is at the precipice of this chasm in 2020.

How can we Cross the Chasm?

Source: Aidos Inc.; Key Hurdles for Crossing the DeFi Chasm.

Concretely, there are four key hurdles to the mass adoption of DeFi.

First, the DeFi ecosystem needs standard Developer Tools and APIs allowing the creation, testing, and deployment of enterprise and consumer decentralized apps or dApps.

Furthermore, front-end web tech and UX/UI need to allow for the seamless integration with these dApps, allowing for a more nimble and agile product development process.

Second, we need to tackle the fundamental problem of Scalability.

It is absurd that in this day and age where Neuromorphic Computing is a reality, that Bitcoin is operating at an embarrassing rate of 4 transactions per second or tps (Ethereum is not any better at 10 tps).

Many potential solutions have been suggested to overcome this hurdle, but what we need is a consensus and a leader to emerge, which may very likely come from a well-capitalized incumbent like J.P. Morgan providing the financing for an external, startup project.

With increased scalability, this will lead to enhanced trading volume and improved Liquidity, leading to better price discovery and fairer transactions for all participants.

Third, many of the shortcomings of Blockchain 1.0 (i.e., Bitcoin) has stemmed from a lack of Governance, and I'm excited to see solutions being developed around this critical issue to say improve the process around the Bitcoin Improvement Proposals (BIPs).

Fourth, Data Transparency and User Privacy is of paramount importance in order to build trust in the technology and organically grow the DeFi ecosystem.

With the fallout of many ICO scams, Blockchain's reputation has taken a nosedive, and in order to gain mass adoption, we need to embed structural features into blockchains allowing for the delicate balance between transparency and personal user privacy.

Final Thoughts

Decentralized Finance is the natural evolution of Finance and signals a secular shift away from an archaic model of intermediated finance to a more decentralized approach that will usher in a new era of FinTech 2.0 during this decade of the Roaring 2020s.

Although there remains many issues from a regulatory, liquidity, governance, and execution perspective, DeFi continues to show much promise for enhancing the efficiency and reducing economic frictions within the financial markets.

Indeed, Blockchain is but just another building block for FinTech and I hope with some of the ideas from this guide, you're well on your way to spreading the DeFi philosophy, and implementing a comprehensive Digital Assets Strategy for your own organization.

I believe it will be well worth it.

By Andrew Vo,

Editor of The Humble Guide

About The Humble Guide

The Humble Guide is a new kind of publication that cuts through the noise of venture capital and technology. Learn what really matters from a thought leader with over a decade of experience in finance, technology, and early-stage investing.

👉 If you enjoyed reading this post, feel free to share it with friends!

To read more content like this every week, subscribe to The Humble Guide 👇