Diversity Matters in Venture Capital

Diversity Matters in Venture Capital

The Humble Guide | Insight Piece #3

Here is the "secret menu" metaphor I often use when asked by many to describe the current state of diversity in Venture Capital:

If you go to an authentic Chinese restaurant in a large city like New York or San Francisco, and if you're not Chinese, they will give you a standard menu that has items in both English and Chinese.

But if you're Chinese, they'll give you a different menu. Often it's a menu that is completely in Chinese and has special items that aren't on the standard menu.

If you replace Chinese with "American" and restaurant with "Venture Capital", you get a disturbingly accurate picture of the current landscape of diversity in venture capital.

As this op-ed may be contrary to popular belief, I ask that you please suspend any judgment or emotional biases before finishing the reading or have studied the diversity data behind venture capital, which is unfortunately opaque and quite limited.

If you find any gap in what I am saying, please don't conclude against me, because in a brief amount of words, I am trying to convey some very disturbing realities that exist in the venture capital ecosystem. Please don't confuse my lack of knowledge with lack of truthfulness.

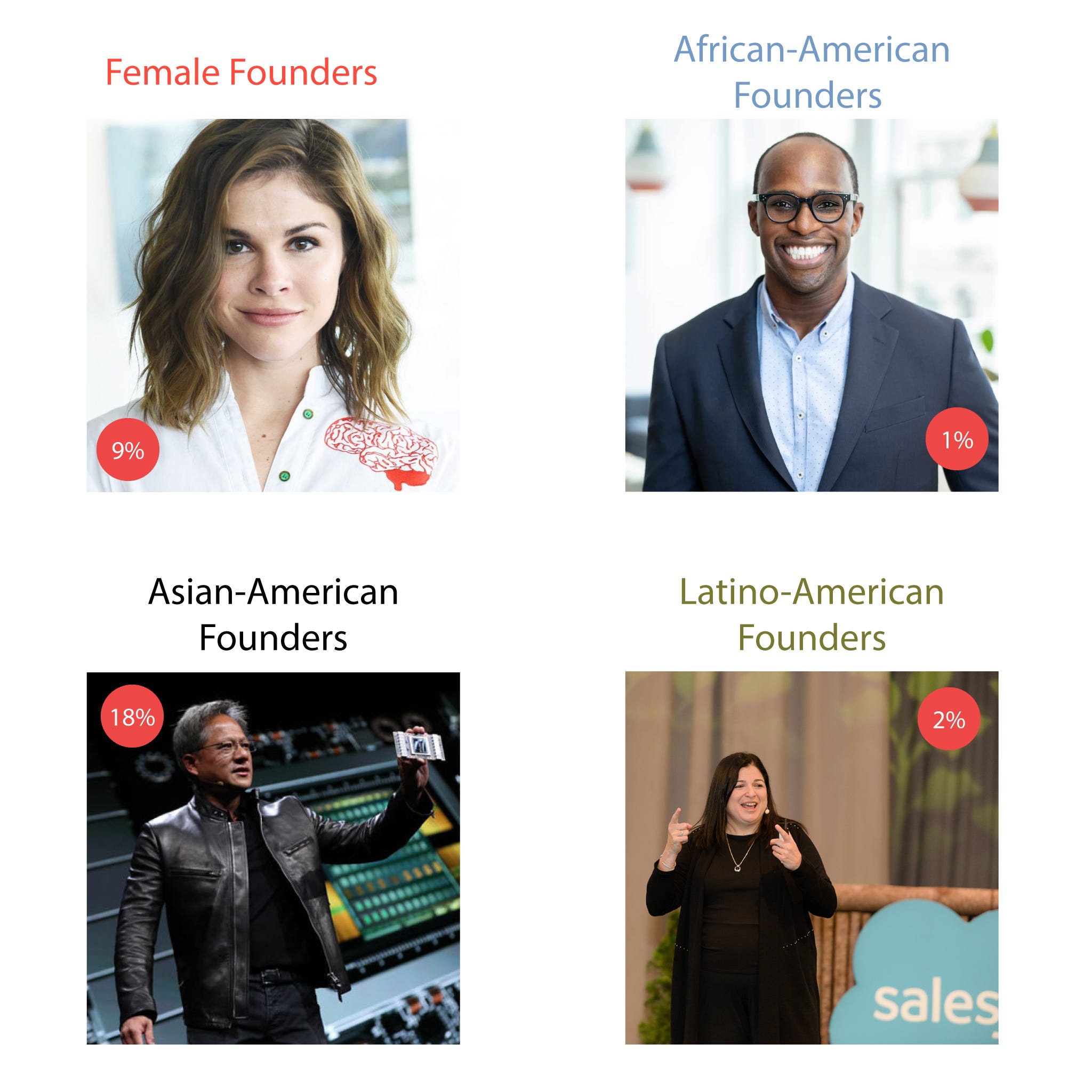

Diversity in Venture Capital by the Numbers

Based on a recent study by RateMyInvestor and DiversityVC, which can be found here, of the 10,000 Founders in the past five years for U.S. venture-backed startups, over 70% of the Founders are Caucasian Men, with the remaining 30% consisting of:

Female Founders: 9% or 900 Women

African-American Founders: 1% or 100 African-Americans

Latino-American Founders: 2% or 200 Latino-Americans

Asian-American Founders: 18% or 1,800 Asian-Americans

Source: Aidos Inc., RateMyInvestor, DiversityVC; Diversity study of 10,000 Founders in the past five years for U.S. venture-backed startups reveals startling statistics.

These numbers are disturbing indeed, but can Diversity Investing improve investment returns, as measured by investment metrics like IRRs (internal rate of returns) and MOICs (money on invested capital), for a VC's underlying investors - the limited partners or LPs?

We believe so, but it requires redefining what "Diversity" means.

Diversity Covers Multiple Dimensions

As a former portfolio manager at J.P. Morgan, my investment team was responsible for managing USD 10 billion of investments for large asset owners like pensions, endowments, sovereign wealth funds, and family offices.

My investment team often had to pass on client mandates because we consistently outperformed our peers in "multi-asset total return investing", which simply meant we were very skilled at investing our client's assets across both public and private market assets.

If you had to ask me what was the key to our success as investment managers, I would point to our ability to truly understand the "Fundamental Law of Active Management."

In a seminal paper published in 1997 on the "Seven Quantitative Insights into Active Management Part 3: The Fundamental Law of Active Management", the Author

Ronald Kahn argues that the productivity of an Active Investment Manager will depend both on (1) his level of skill, and (2) how often that skill is put to use.

Nothing could be more true than that.

The idea and resulting equation are simple enough.

An active investment manager produces Information Ratio (IR), which is a measure of the value-added per unit risk. His skill in producing IR is defined by the Information Coefficient (IC), and the extent to which he applies his skill is termed "Breadth", which is defined as the number of independent signals he derives.

IR = IC * sqrt(Breadth)

This single formula is the engine that drives Trillions of Dollars in assets that are managed by thousands of active asset managers globally, including Goldman Sachs, J.P. Morgan, UBS, Amundi, BlackRock, and Blackstone.

Applying this formula to venture capital investing is a bit nuanced since we're dealing with direct investments in early-stage companies where the success of the investment depends on individual Founders.

That said, don't think of Diversity purely as a social or philanthropic mechanism to allocate capital to a certain percentage of Women, Minorities, LGBT, Disabled, or Veteran Founders.

Instead, a more insightful definition of Diversity encompasses something more expansive and more fundamental, which will provide insights into enhancing venture capital returns.

Within the context of Venture Capital Investing, Diversity is the value-added benefits of combining complementary Founder Backgrounds and Life Perspectives to build exceptional early-stage businesses.

Source: Aidos Inc.; Aidos defines Diversity as a mix of Backgrounds and Life Perspectives.

Great, so Diversity is correlated to Breadth within the context of venture capital investing.

The natural question now arises: does this new definition of Diversity Investing generate above-average returns for investors relative to traditional "Non-Diverse Investing"?

Diversity Investing Enhances Investment Returns

We believe so, and the numbers back it up.

Source: Aidos Inc.; Diversity Investing can generate superior risk-adjusted returns.

On the Investment side:according to a seminal whitepaper on "The Other Diversity Dividend" (published by the Harvard Business Review here), by examining the decisions of thousands of venture capitalists and tens of thousands of investments, Diversity significantly improves financial performance on measures such as profit, EBITDA, and return on equity.

On the Investing side: according to a recent study of "Women in the Venture Capital Ecosystem" (published by PitchBook here), although 12% of decision-makers at U.S. venture capital firms are female, 70% of top-quarterly performing U.S. venture capital funds are led by female-decision makers.

Final Thoughts

Returning to the "secret menu" metaphor.

If you talk to Female and Minority Founders, they will often tell you they've had experiences with venture capital investors that have discouraged them from going on, either because they think their "business is not investible by venture capital, that it's too early-stage, that it lacks product/market fit or traction", or some cookie-cutter reasons.

This is code-speak for the status quo: "Sorry, you don't belong in our inner circle."

So I used the metaphor "secret menu" to mean: Venture Capitalists, do you have a "secret investment checklist" and who gets to see this checklist?

Do you share this secret menu with your underlying investors?

Ironically, the investors or "limited partners" are typically public pension funds representing a multi-ethnic group of government employees - the same diverse group of people, which includes exceptionally talented Founders with dreams of starting a company, that venture capitalists won't back because they "don't fit the fund's investment thesis."

Founders of Diverse backgrounds: the next time you get a "No" from a venture capital investor, and the answer sounds vague and ambiguous...

I urge you to ask about their "secret menu."

By Andrew Vo

Editor of The Humble Guide

About The Humble Guide

The Humble Guide is a new kind of publication that cuts through the noise of venture capital and technology. Learn what really matters from a thought leader with over a decade of experience in finance, technology, and early-stage investing.

👉 If you enjoyed reading this post, feel free to share it with friends!

To read more content like this every week, subscribe to The Humble Guide 👇